Homeonwers on the verge of foreclosure will often seek a short sales as a graceful exit from otherwise calamitous financial situation. Their homes are sold for less than the mortgage amount, and the remaining loan balance is usually forgiven by the lender.

http://www.nytimes.com/2010/02/28/realestate/28mort.html

Wednesday, March 3, 2010

Monday, February 22, 2010

Monday, February 15, 2010

New ‘Good Faith’ Takes Hold

By BOB TEDESCHI, New York Times

Published February 9, 2010

Published February 9, 2010

FEW mortgage borrowers have had the fortitude for a thorough reading of all their loan paperwork, often feeling intimidated or overwhelmed by the legalese and numerical complexities in the disclosures. But some mortgage brokers say that such passivity is declining.

"Consumers are much more involved in the process than in the past," said Richard Martin, a senior vice president with DE Capital Mortgage in New York, adding that not all of his clients may want to be as engaged. "But if you want to be protected, you've got to be involved."

Starting Jan. 1, lenders and brokers were required to provide borrowers with new Good Faith Estimate forms, which were simplified from years past, to show the final closing costs, and the maximum rate a borrower might pay on variable loans, among other things. Borrowers are asked to sign the document and return it to lenders and brokers before the underwriting process can begin.

"That's brought about an increase of 50 percent in the number of inquiries we're getting on these documents," Mr. Martin said.

Research shows that, in the past at least, the dialogue between lenders and borrowers was often sparse. According to a survey of loan officers fielded late last year and released last month by Wolters Kluwer Financial Services of Minneapolis, 36 percent of borrowers asked five questions or fewer during the loan process.

The borrowers may have been so well informed that they did not need to ask questions, but many mortgage brokers and industry executives suspect the opposite.

"Consumers don't understand this stuff," said Brian Benjamin, the president of Two River Mortgage and Investment in Red Bank, N.J. "People will say, 'Just do what you think is right,' but 10 percent of all the people in the industry" are not to be trusted, in his estimation.

Still, Mr. Benjamin says the new disclosure forms have not necessarily helped make borrowers more active participants in the loan process. In fact, he believes the new system has replaced confusion of one kind with confusion of another. Clients have been asking roughly the same number of questions as in the past, but now they ask more questions pertaining to closing costs not itemized in the new disclosure form, he said.

Mr. Benjamin suggested that borrowers also request to see the loan costs broken down on an old version of the Good Faith Estimate, for a more detailed accounting of the loan's costs.

The new Good Faith Estimate has also increased the amount of time it takes to close a loan, some industry executives say.

Mr. Martin of DE Capital says the new disclosure form has added five days to the time it takes to process a typical loan. That is because lenders must seek fee quotations from third parties like title companies and lawyers before sending the form to the borrower.

Guaranteed quotations are important for brokers and lenders, because closing costs must remain posted until the final estimate, which is given three days before the settlement date. If, during the processing of the loan, the costs change the effective rate of interest by one-eighth of a percentage point, a new set of disclosure documents must be issued, and the loan cannot close for at least another three days after that point.

After issuing the first Good Faith Estimate, lenders must wait for borrowers to sign and return the document before ordering an appraisal. That extra time pushes the loan approval process to at least 45 days, up from the typical 40, forcing some borrowers to pay extra fees to guarantee an interest rate, Mr. Martin said.

And these extra fees, he added, can easily add a quarter of a percentage point to the interest rate.

Stager's Corner

Debbie Oulvey, creator of Amazing Space NYC LLC, brings an Interior Design and a business background to her Real Estate Staging business. Debbie, a Real Estate Stager was featured in the November 2009 Real Notes issue.

Here are two examples of her work, showing before and after photos:

Living Room Before

Living Room After

Bedroom Before

Bedroom After

Debbie Oulvey – ASID, CSP, RESA

Amazing Space NYC LLC

http://www.amazingspacenyc.com/

917.428.3965

Here are two examples of her work, showing before and after photos:

Living Room Before

Living Room After

Bedroom Before

Bedroom After

Debbie Oulvey – ASID, CSP, RESA

Amazing Space NYC LLC

http://www.amazingspacenyc.com/

917.428.3965

Mortgage Matters

Adam W. Turkewitz, CMPS, Private Mortgage Banker

Wells Fargo Home Mortgage

530 Fifth Avenue, 15th Floor

New York, NY 10036

(212) 805 1172 Office, (516) 456-3687 Mobile

adam.turkewitz@wellsfargo.com

Wells Fargo Home Page

Advertising Review

In this column we show some of the more interesting aspects of ads. What does and does not work and why? Consider this photo from a recent walk up listing in Greenwich Village:

What thoughts come to your mind when looking at this picture? Perhaps the single most important aspect that stands out here is how much sun is coming in through the windows. Third floor walk up apartments in the Village are not known for being bright so this is a rare quality that needs to be showcased. What about the photo below?

What thoughts come to mind here? Which positive features are being highlighted? This is a photo from a recently posted ad by an owner selling his own apartment in Manhattan. Buyers and agents look at pictures like this and see weakness than can be exploited in negotiations. They are correct to assume that this picture does nothing to educate or motivate the audience to visit or bid on this apartment. As a result the closing price will probably be much less than market value.

What thoughts come to your mind when looking at this picture? Perhaps the single most important aspect that stands out here is how much sun is coming in through the windows. Third floor walk up apartments in the Village are not known for being bright so this is a rare quality that needs to be showcased. What about the photo below?

What thoughts come to mind here? Which positive features are being highlighted? This is a photo from a recently posted ad by an owner selling his own apartment in Manhattan. Buyers and agents look at pictures like this and see weakness than can be exploited in negotiations. They are correct to assume that this picture does nothing to educate or motivate the audience to visit or bid on this apartment. As a result the closing price will probably be much less than market value.

What's Missing?

Real Estate marketing has one chance to make a good first impression. Missing or wrong information leads buyers and their agents to feel either the person responsible for the ad is either incompetent, dishonest or both.

Savvy buyers understand that others are also seeing this mistake and as a result are less likely to bid market price. They see one weakness in the seller's position and eagerly look for others to assess how low a price the property is likely to close for. If buyers think the ad is a deliberate attempt to mislead the public they will distrust other things the seller is saying i.e. what the actual maintenance is, building features etc. In either case the credibility of the asking price is compromised.

Real Estate marketing can be broken down into basic elements:

1) Facts. These include the asking price, monthly charges, minimum financing requirements, address, building type (Coop, Condo or Condop).

2) Description. These sentences describe the location, building and apartment's most desirable features.

3) Photos. If a picture is worth a thousand words then this is the most important and best value way to spend advertising money. Pictures are not only another way to show the apartments best features but in some cases the only option. If the description says the living room get excellent light all day and the pictures don't show this, what will the buyer think? Experienced agents know that if the photos don't show something, there's probably a good reason.

4) Floor Plans. It's important to show reasonably accurate dimensions and scale. This is also a chance for sellers to show the public alternate layouts - perfectly ok as long as they are labeled as such.

Thursday, February 11, 2010

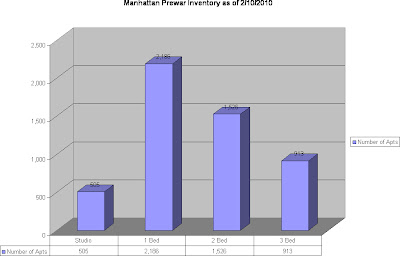

The State of the Market

One of the constants about the Manhattan residential market is its seasonality. Certain types of apartments sell better as the weather warms than they do in the middle of the winter. Studio and one bedroom activity increases, particularly downtown, as students graduate from college and need to get established for their new jobs. Outer lying areas (avenues near the East River or Hudson River) can benefit from better weather because they seem more accessible to buyers.

The chart below is a snap shot of all Coops and Condos available in Manhattan as of February 10, 2010.

The overall numbers here have been consistent for the past month with new apartments on the market somewhat being balanced by signed contracts. We continue to carefully monitor the status of signed contracts as an indication of the degree of difficulty in getting residential mortgages. The past 12 months have shown this to be by far the single biggest challenge facing sellers today. The discrepancy between the number of studios and one bedrooms available can be partially explained by first time buyer activity. The price decreases in this area have made this part of the market affordable for buyers who have been priced out for the past several years. Another important factor is that new Condo construction usually consists of one bedrooms and larger sized apartments and rarely includes studios.

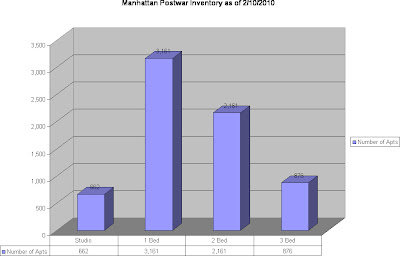

We've included the 2 charts below to show that the number of apartments built before World War II continues to lag behind modern construction.

The chart below is a snap shot of all Coops and Condos available in Manhattan as of February 10, 2010.

The overall numbers here have been consistent for the past month with new apartments on the market somewhat being balanced by signed contracts. We continue to carefully monitor the status of signed contracts as an indication of the degree of difficulty in getting residential mortgages. The past 12 months have shown this to be by far the single biggest challenge facing sellers today. The discrepancy between the number of studios and one bedrooms available can be partially explained by first time buyer activity. The price decreases in this area have made this part of the market affordable for buyers who have been priced out for the past several years. Another important factor is that new Condo construction usually consists of one bedrooms and larger sized apartments and rarely includes studios.

We've included the 2 charts below to show that the number of apartments built before World War II continues to lag behind modern construction.

Tuesday, January 19, 2010

Mortgage Matters by Adam Turkewitz

530 Fifth Avenue, 15th Floor, New York, NY 10036

(212) 805 1172 Office (516) 456-3687

Mobile (646) 253-7788 Fax

adam.turkewitz@wellsfargo.com

https://www.wfhm.com/loans/adam-turkewitz/index.page

Thursday, January 7, 2010

Get It Appraised

One of the tactics found very useful in the past 2 years has been getting apartments independently appraised by an outside firm before they come to market. You may already be aware of the fact that when a buyer applies for a mortgage (or refinance) an appraiser is sent to prepare an in depth analysis of comparable closed apartments, the current market, building financials etc. to come to a conclusion about what an apartment is worth. Due to the credit crunch many deals in Manhattan have come apart because the price an appraiser came up with was lower than the contract price.

By getting an apartment independently appraised owners can avoid this problem and get a more objective view quickly. This can not only save considerable time, effort and quite a bit of money because the market may still be in flux. Having an appraisal in hand is also a very powerful negotiating tool with buyers and other agents. A listing price is more likely to be respected if it's supported by a source outside of the exclusive broker.

This is not a wide spread tatic at the sub $1,000,000 level but common with properties in the $2M and up range. Every owner should consider doing this even if the property is on the less expensive end of the market. It's not a step that many sellers attorneys agree with yet because it costs money - usually in the range of $500-$1,000. All interested parties will begin to understand the rules for how transactions flow must be re-written because of the changes in the banking realm.

By getting an apartment independently appraised owners can avoid this problem and get a more objective view quickly. This can not only save considerable time, effort and quite a bit of money because the market may still be in flux. Having an appraisal in hand is also a very powerful negotiating tool with buyers and other agents. A listing price is more likely to be respected if it's supported by a source outside of the exclusive broker.

This is not a wide spread tatic at the sub $1,000,000 level but common with properties in the $2M and up range. Every owner should consider doing this even if the property is on the less expensive end of the market. It's not a step that many sellers attorneys agree with yet because it costs money - usually in the range of $500-$1,000. All interested parties will begin to understand the rules for how transactions flow must be re-written because of the changes in the banking realm.

1031 Like-Kind Exchanges

Tax deferred exchanges have long been a means of shielding investors from capital gains tax on the sale of real property. As real estate prices continue to climb, so do the gains and therefore the tax liability investors face. Familiarity with tax deferred exchanges is not only a useful tool, but a requirement for anyone advising clients selling business or investment properties.

The delayed exchange process can be broken down into three steps:

1. The exchanger sells the relinquished property.

2. The exchanger identifies the replacement properties within 45 days following the sale of the

relinquished property.

3. The replacement property must be acquired by the exchanger by the earlier of 180 days following the sale of the relinquished property or the date the taxpayer must file its tax return (including

extensions) for the year of the transfer of the relinquished property.

As part of the exchange, an intermediary must be involved to incorporate the exchange documentation. The

intermediary assigns into the transaction to maintain the essence of an exchange. Additionally, the intermediary retains the exchange proceeds during the exchange process, as the taxpayer must avoid receipt of any exchange proceeds for full tax deferral treatment.

Furthermore, the relinquished and replacement property must be held for investment or productive use in a trade or business. The eligibility of an investment property is assessed based on the intent of the taxpayer. Real property held as a primary residence or for resale purposes does not qualify. The duration a property is held is one factor in assessing a taxpayer's intent, along with other facts and circumstances of a situation. Some advisors recommend that taxpayers hold property for a minimum of one-year as an investment property, while others recommend a more conservative two-year hold.

Many exchangers incorrectly assume they are able to acquire a replacement property equivalent to their basis in the relinquished property. To avoid surprise tax bills, the exchanger must apply all the net proceeds towards the purchase of a replacement property of equal or greater value to that of the property sold, or pay the tax on the difference.

The benefits of an exchange are not limited to individual taxpayers. However, the tax code requires, with very limited exception, that the exchanging entity be the same entity acquiring replacement property. Whether the entity is a corporation, a partnership or a limited liability company, it may achieve a valid exchange as long as the entity remains the owner of the replacement property (assuming the other requirements are also met).

Real estate exchanges are a valid tax tool allowing investors to build their wealth in real estate. The investor is

able to defer the tax liability and reinvest the monies in a new investment or business property. The exchange

process allows for product and geographic diversification as investors exchange into varied forms of real

property (e.g., rental apartment, office, shopping center, etc.) in varying regions of the country. Real estate

advisors must be aware of the benefits of a tax deferred exchange to assist their clients in identifying opportunities to benefit from the exchange process.

LAW OFFICE OF JOHN P. BRADBURY

Five Penn Plaza, 23rd Floor Phone: (212) 697-3529

New York, New York 10001 Fax: (212) 202-5046

jbradbury@nyrelaw.com http://www.nyrelaw.com/

This information is not intended to replace qualified legal and/or tax advisors.

Every taxpayer should review their specific transaction with their own legal and/or tax counsel.

The delayed exchange process can be broken down into three steps:

1. The exchanger sells the relinquished property.

2. The exchanger identifies the replacement properties within 45 days following the sale of the

relinquished property.

3. The replacement property must be acquired by the exchanger by the earlier of 180 days following the sale of the relinquished property or the date the taxpayer must file its tax return (including

extensions) for the year of the transfer of the relinquished property.

As part of the exchange, an intermediary must be involved to incorporate the exchange documentation. The

intermediary assigns into the transaction to maintain the essence of an exchange. Additionally, the intermediary retains the exchange proceeds during the exchange process, as the taxpayer must avoid receipt of any exchange proceeds for full tax deferral treatment.

Furthermore, the relinquished and replacement property must be held for investment or productive use in a trade or business. The eligibility of an investment property is assessed based on the intent of the taxpayer. Real property held as a primary residence or for resale purposes does not qualify. The duration a property is held is one factor in assessing a taxpayer's intent, along with other facts and circumstances of a situation. Some advisors recommend that taxpayers hold property for a minimum of one-year as an investment property, while others recommend a more conservative two-year hold.

Many exchangers incorrectly assume they are able to acquire a replacement property equivalent to their basis in the relinquished property. To avoid surprise tax bills, the exchanger must apply all the net proceeds towards the purchase of a replacement property of equal or greater value to that of the property sold, or pay the tax on the difference.

The benefits of an exchange are not limited to individual taxpayers. However, the tax code requires, with very limited exception, that the exchanging entity be the same entity acquiring replacement property. Whether the entity is a corporation, a partnership or a limited liability company, it may achieve a valid exchange as long as the entity remains the owner of the replacement property (assuming the other requirements are also met).

Real estate exchanges are a valid tax tool allowing investors to build their wealth in real estate. The investor is

able to defer the tax liability and reinvest the monies in a new investment or business property. The exchange

process allows for product and geographic diversification as investors exchange into varied forms of real

property (e.g., rental apartment, office, shopping center, etc.) in varying regions of the country. Real estate

advisors must be aware of the benefits of a tax deferred exchange to assist their clients in identifying opportunities to benefit from the exchange process.

LAW OFFICE OF JOHN P. BRADBURY

Five Penn Plaza, 23rd Floor Phone: (212) 697-3529

New York, New York 10001 Fax: (212) 202-5046

jbradbury@nyrelaw.com http://www.nyrelaw.com/

This information is not intended to replace qualified legal and/or tax advisors.

Every taxpayer should review their specific transaction with their own legal and/or tax counsel.

Subscribe to:

Posts (Atom)